Africa’s iGaming industry is evolving rapidly, with several markets across Sub-Saharan Africa moving beyond “emerging” status into structured, regulated, and commercially viable ecosystems.

While South Africa has traditionally dominated conversations around gaming on the continent, attention is increasingly shifting to other high-potential markets. Nigeria, Kenya, Angola, and Ghana are now at the center of this transformation, each offering unique growth opportunities shaped by regulation, technology, and user behaviour.

These markets are not only active but increasingly attractive for operators and investors who understand how to navigate their local dynamics.

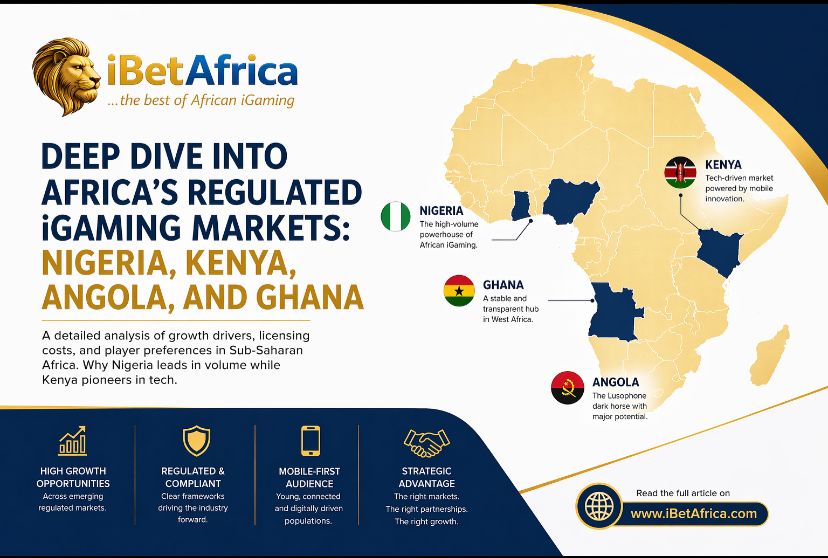

Nigeria remains the largest iGaming market in Sub-Saharan Africa, driven by its population size, strong mobile adoption, and deep-rooted passion for sports betting. With over 200 million people and a highly engaged betting audience, the country continues to lead in volume.

However, the regulatory landscape presents a level of complexity. Operators must navigate both federal oversight, led by the National Lottery Regulatory Commission (NLRC), and state-level authorities such as the Lagos State Lotteries and Gaming Authority (LSLGA).

Licensing costs are significant, with federal sports betting licenses reaching approximately ₦100 million, alongside an 11% tax on Gross Gaming Revenue introduced in 2026. Despite these challenges, the market remains highly attractive due to its scale.

Mobile usage dominates, with the vast majority of bets placed via smartphones. While sports betting leads, there is growing interest in crash games and virtual sports, reflecting evolving user preferences and increasing openness to new gaming formats.

Kenya stands out as one of Africa’s most technologically advanced iGaming markets, largely due to its early adoption of mobile money systems such as M-Pesa.

The country’s payment infrastructure is deeply integrated into the betting experience, allowing for near-instant deposits and withdrawals. This efficiency has contributed to a high level of user trust and engagement.

Regulation is managed by the Gambling Regulatory Authority (GRA), which has introduced stricter licensing requirements and player protection measures. Operators are required to meet capital thresholds, provide security guarantees, and comply with evolving tax frameworks.

Kenya’s taxation model has shifted toward a transaction-based system, where levies are applied to both deposits and withdrawals. While this increases operational pressure, it also ensures consistent government revenue and regulatory transparency.

The Kenyan player base is highly informed and digitally literate, with strong expectations around platform performance, speed, and payout efficiency. This makes the market competitive but rewarding for operators that deliver a seamless experience.

Angola is emerging as one of the continent’s most promising yet underexplored markets.

Often overlooked due to language differences, the country presents a unique opportunity for operators willing to localize their approach for Portuguese-speaking audiences. Recent regulatory developments have further strengthened its appeal.

The introduction of a new gaming law in 2025 has created a more structured and forward-looking framework, with online licenses offering long-term validity and increased clarity for operators. The regulator has also begun accepting new applications, signalling a more open and progressive stance toward market participation.

With a population of over 40 million and growing internet penetration, Angola offers a less saturated environment compared to its English-speaking counterparts. However, success in this market requires strong localization, particularly in language, user experience, and product positioning.

Ghana continues to position itself as one of the most stable and transparent iGaming markets in West Africa.

Regulated by the Gaming Commission of Ghana, the country provides a structured environment that supports long-term planning and investment. Licensing requirements are clearly defined, with foreign operators expected to meet minimum capital thresholds.

Taxation remains relatively high, with a 20% levy on Gross Gaming Revenue. However, the removal of the withholding tax on player winnings in 2025 has improved market attractiveness and user participation.

Demographically, Ghana benefits from a young, mobile-first population that is highly receptive to digital platforms. This creates strong opportunities for operators focusing on user experience, social features, and mobile optimization.

Despite the opportunities across these markets, success in Africa’s iGaming industry requires more than market entry. It demands a deep understanding of local realities.

Operators must address key technical and operational challenges, including high data costs, network limitations, and the need for fast, reliable payment systems. Lightweight platforms, efficient content delivery, and instant payout capabilities are no longer optional but essential for competitiveness.

Equally important is trust. In markets where users are highly sensitive to payment reliability, platforms that deliver consistent and transparent experiences are more likely to retain users and build long-term loyalty.

Africa’s iGaming landscape is not a single market but a collection of distinct ecosystems.

Nigeria offers unmatched scale. Kenya leads in payment innovation and user sophistication. Angola provides a gateway into an underserved Lusophone market. Ghana delivers stability and regulatory clarity.

For operators and investors, the opportunity is clear. However, the winners will be those who move beyond a one-size-fits-all approach and build strategies tailored to each market’s unique structure.